Selling a Home With an ADU: Permits, Disclosures, Appraisals and Liability Risks

Accessory Dwelling Units (ADUs) are becoming more common in residential real estate. Driven by housing affordability challenges, multigenerational living, and demand for flexible space, ADUs are increasingly part of how properties are marketed and valued. Federal housing research has also identified ADUs as a potential solution to housing supply constraints, with policy changes in many states encouraging their development.

At the same time, ADUs introduce complexity that many transactions are not prepared for.

The ADU itself can become an issue not because of the structure alone, but because of everything connected to it. Permits, zoning, rental use, valuation, and disclosure all come into play, and when what is marketed, permitted, valued, and disclosed does not align with what the buyer ultimately receives or understands, that is where risk begins.

Quick Takeaways

- An ADU must meet local zoning and permit rules to be considered legal

- Disclosure is the biggest source of risk

- ADUs do not automatically increase property value

- Rental income is not guaranteed or always usable for financing

- Most claims come from misrepresentation or missing information

The First Question: Is the ADU Legal?

An ADU is considered legal only if it complies with local zoning and permitting requirements, which directly affects how it can be marketed, financed, and insured.

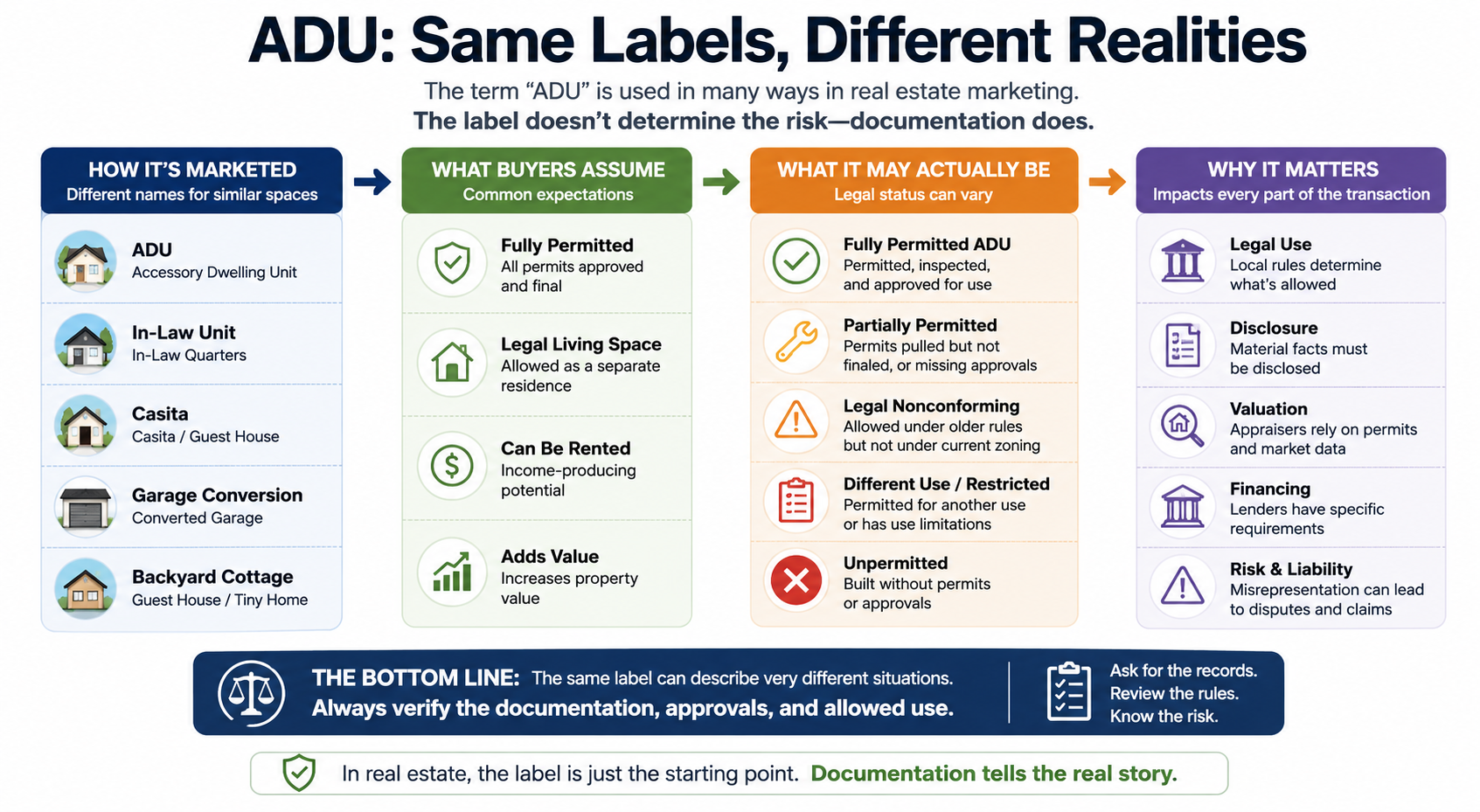

An ADU may exist on a property, but that does not mean it is legally recognized. In some cases, the unit was built with full permits and approvals. In others, it may be partially permitted, built without permits, or created under older rules that no longer apply. It may also meet zoning requirements but lack final approval.

This distinction matters because legal status affects how the property can be marketed, financed and valued.

If a unit does not meet local zoning or permitting requirements, it may be treated differently in the appraisal process or raise additional eligibility considerations, as noted by Fannie Mae’s property eligibility guidance. The key issue is not whether the space exists, but whether its use, condition and description are supported by how the property is documented.

That is why clarity around permits and zoning is so important early in the process. It sets the foundation for how the rest of the transaction will be understood.

Where Claims Begin: Disclosure Failures

Real estate professionals must disclose any known facts about an ADU that could affect a buyer’s decision or the property’s value. This is where risk most consistently concentrates.

Real estate claims often hinge on whether buyers receive complete and accurate information. With ADUs, there are simply more details that can affect how a property is understood.

This may include permit history, whether approvals were finalized, how the space has been used, and any known limitations tied to zoning or occupancy. It can also involve explaining differences in square footage, bedroom count or utility setup.

ADUs are especially prone to gaps because they are often modified over time. A garage may have been converted without full documentation, a space may have been rented informally, or improvements may have been made in stages with mixed permitting.

When a buyer discovers after closing that the unit was not permitted as expected, cannot be used as described, or carries limitations that were not clearly communicated, the issue shifts from the property itself to how it was represented. That is where many disputes begin.

Claims data from real estate professional liability insurers consistently shows that misrepresentation and incomplete disclosure are leading causes of claims, particularly in transactions involving complex property features.

Buyers should be encouraged to verify permits, zoning, and use restrictions independently, especially when information is incomplete or unclear.

The Appraisal Gap: When Value Does Not Match the Story

An ADU does not automatically increase property value. How much it adds, if anything, depends on market demand, whether the unit is permitted, and how it compares to similar properties.

Data from the Federal Housing Finance Agency shows that properties with ADUs in some markets have seen stronger value growth over time. Not every property with an ADU will be valued higher.

Appraisers rely on comparable sales and market data. They must identify and analyze the ADU based on how it is permitted and how similar properties are treated, as outlined in Fannie Mae’s appraisal guidance. If the unit is not permitted or does not meet local requirements, it may be treated differently or contribute less to the overall value.

If a property is marketed as adding significant value, but the appraisal does not support that conclusion, buyers and sellers may have very different expectations. This can lead to renegotiation, financing challenges, or disputes after closing.

The key takeaway: an ADU may add value, but it does not guarantee a higher price. Its impact depends on how the market views it and how it is documented and evaluated.

Rental Income: Where Expectations Often Outpace Reality

Rental income is one of the most commonly marketed benefits of ADUs, but it is also one of the most misunderstood.

A common question is whether rental income from an ADU can be used to qualify for a mortgage. The answer is sometimes, but only if it meets documentation and eligibility requirements. Guidance from the Department of Housing and Urban Development (HUD) and Freddie Mac requires that income be supported, consistent, and allowable under program rules, with limits on how much can be counted and when it can be used.

There is also a difference between a space that could be rented, one that has been rented, and one that qualifies as income for lending purposes.

Local regulations further complicate this. Short-term rentals may be restricted, require minimum stays, or limit how the property can be used, which can directly affect income potential.

Rental income is not guaranteed. It depends on how the ADU is permitted, documented, and evaluated under lending and local rules.

Risk increases when marketing presents rental income as certain. Phrases like “income-producing unit” or “rental-ready ADU” can create expectations that may not hold up during underwriting or after closing.

When those expectations are not met, the gap between what was implied and what is achievable can lead to financing issues or disputes.

Marketing Language vs Verifiable Reality

In ADU transactions, risk is rarely created by the structure itself. It comes from the difference between how the property is described and what can be verified.

Real estate marketing often uses short phrases that carry strong meaning. Terms like “fully permitted ADU,” “separate residence,” or “income-producing unit” suggest approval, usability, and value that buyers may rely on.

Those statements are only accurate if they are supported by documentation. If a unit is described as fully permitted, there should be a clear permit history and final approvals. If it is presented as a separate residence or income-producing, zoning, occupancy, and lending standards should support that use.

Risk increases when those claims go beyond what can be supported, especially as listings are repeated across MLS platforms, websites, and social media.

If those expectations are later challenged by appraisal results, lender requirements, or local regulations, the issue shifts from the property to how it was represented.

What Counts as an ADU and Why the Definition Matters

The term “ADU” is used broadly in real estate marketing. It can refer to a detached structure, a converted garage, a basement apartment, or an attached living space. Listings may also use terms like “in-law unit,” “casita,” or “garage conversion” to describe similar spaces, and Freddie Mac includes many of these under the same category.

The label itself does not determine risk. What matters is how the space is recognized and documented.

A unit may be fully permitted, partially permitted, built for a different use than how it is described, or not permitted at all. These differences affect how the property can be used, valued, and disclosed.

When the label does not match the documentation, risk increases.

Why ADU Risk Is Highly Local

ADU rules are set at the local level, which means zoning, permitting, and use restrictions can vary significantly from one jurisdiction to another.

A unit that is allowed in one area may face limitations or require additional approvals in another. Local rental rules can also affect how the unit is used, including restrictions on short-term rentals, minimum stay requirements, or occupancy rules. Buyers should also be aware of any proposed changes to these regulations, as they can directly impact future use and income.

Because of this variability, assumptions based on prior experience can be misleading. Each property must be evaluated based on the rules that apply to its specific location.

How ADU Issues Turn Into E&O Claims

When ADU-related disputes arise, they often follow a similar pattern.

A buyer evaluates a property based in part on how the ADU is described. That description can shape expectations around value, intended use, or rental income. After closing, the buyer discovers that the unit does not align with those expectations.

The issue may involve permitting status, zoning limitations, rental restrictions, or the cost required to bring the unit into compliance. In some cases, it may also involve substandard construction, such as work completed without proper licensing, poor workmanship, or improvements that do not meet code requirements.

The focus shifts from the property to how it was represented. Questions arise around what was known, what was communicated, and whether key details were omitted or overstated.

Industry claims data shows that many disputes are driven by misrepresentation or incomplete disclosure, reinforcing the idea that liability often stems from how property information is communicated rather than the property itself

Because permitting, use, valuation, and construction quality can all vary, the likelihood of misunderstanding increases. That is what makes these transactions particularly sensitive from a liability perspective and central to real estate professional liability and E&O insurance considerations.

A Common ADU Claim Scenario

Consider a common scenario. A property is marketed as having a “fully permitted income-producing ADU,” with the listing highlighting rental potential and added value.

During the transaction, the appraisal does not support the expected increase in value, and the lender limits how rental income can be considered. After closing, the buyer discovers the unit lacks final permit approval and cannot be used as expected.

At that point, the issue is no longer about the structure itself. It becomes a question of how the property was represented, what was known, and what the buyer relied on when making the purchase decision.

Reducing Risk When ADUs Are Involved

ADUs do not need to be avoided, but they do require a more deliberate approach.

Reducing risk starts with understanding how the unit is locally permitted and used. This helps set a foundation for how the property can be accurately described.

From there, alignment becomes the priority.

Listing language should reflect what can be supported by available information. Statements about value, legality, or income potential should account for uncertainty where it exists, rather than assume outcomes that may not hold up during appraisal or underwriting.

Clear and consistent disclosure is also critical. Communicating what is known about the ADU, while acknowledging any gaps or limitations, helps ensure buyers have the context needed to evaluate the property.

Buyers should also be encouraged to verify permits, zoning, and use independently, especially when details are unclear or incomplete. If you are a seller's agent, you should have the seller provide signed documentation of these items. Claims often occur months or years after a sale. Documenting all information in writing gives you peace of mind and protects you from E&O claims.

These steps do not eliminate risk entirely, but they can reduce the likelihood that misunderstandings turn into disputes later in the transaction.

The Bottom Line

Accessory Dwelling Units are becoming an increasingly common feature in residential real estate, shaped by changing housing needs and evolving local policies.

They can add flexibility, functionality, and in some cases, value.

The risk is not the existence of the unit. It is the gap between how the unit is represented, how it is documented, how it is evaluated, and how it is ultimately understood by the buyer.

When those elements align, ADUs can enhance a transaction. When they do not, that gap is often where problems begin.

Frequently Asked Questions About ADUs and Real Estate Risk

Can you sell a home with an unpermitted ADU?

Yes, but it may affect value, financing, and disclosure. Unpermitted units may not be recognized by appraisers or lenders, so the key is clearly communicating the unit’s status.

What should be disclosed about an ADU?

Any known facts that could affect a buyer’s decision or value should be disclosed, including permit status, prior use, zoning limitations, and differences in square footage or configuration.

Does an ADU automatically increase home value?

No. An ADU may add value, but it depends on permit status, market demand, and comparable sales. Appraisers rely on market data, not just the presence of the unit.

Can rental income from an ADU be used to qualify for a mortgage?

Sometimes, but only if it meets documentation and lending requirements. Rental income should not be assumed, as it depends on the property and the loan program.

è See the official FAQs page for more information.

Share this page.